LC: AI Capex Flows to Downstream DSP Suppliers

In 2025, large-scale investments in AI infrastructure by mega-enterprises nearly tripled the shipment of 800G PAM4 chipsets, with sales growing by over double year-on-year. These investments continued to rise in 2026, prompting LightCounting to recently revise upward its forecasts for 800G and 1.6T optical transceiver shipments. The current projection indicates that 800G shipments will more than double again in 2026, while 1.6T shipments will expand from a small base in 2025 to tens of millions of ports. Sales of 1.6T chipsets will surpass $2 billion in 2026 and grow rapidly before 2029.

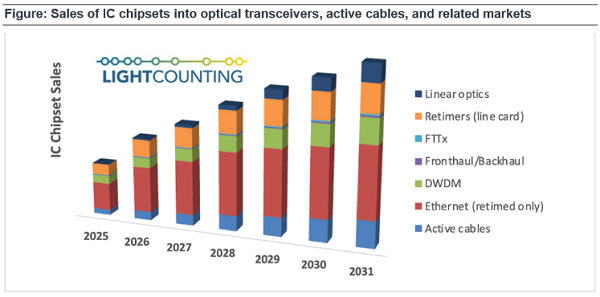

Historically, Ethernet and DWDM have dominated the chipset market. However, the data center market drove rapid growth in chipset sales for active optical cables (AOC/AEC/ACC) and on-board retimers in 2025. During this forecast period, fully retime Ethernet transceivers will continue to contribute the highest dollar growth, followed by active optical cables and linear optical devices (LPO/LRO/CPO).

In 2025, while PAM4 chip sales surged, the sales growth of coherent DSP chipsets was relatively moderate at 16%, primarily driven by demand for DWDM modules. The sales gap between PAM4 chips and coherent chipsets may widen in 2026, mainly due to accelerated adoption of 1.6T PAM4 optical components in AI infrastructure. LightCounting anticipates that the sales growth of PAM4 chipsets will slow down from 2027 to 2031 as the large-scale deployment of linear driving solutions (LPO and CPO) negatively impacts DSP sales. By 2027, shipments of Coherent-Lite may significantly boost coherent DSP sales. Overall, shipments of coherent DSPs are projected to exceed 8 million units by 2031. AI training demand across multiple facilities within data center campuses may drive upward revisions in forecasts, as these workloads require greater inter-building bandwidth.

LightCounting derives historical data on chipset sales from over two decades of collected sales figures for optical transceivers and active cables. Chipset sales forecasts are also based on its projections for optical transceivers and active cables. This approach provides a clear pathway to correlate chipset demand with the deployment of optical connections across various application scenarios. However, it fails to capture the disparities between chipset demand and transceiver demand, which may stem from inventory level fluctuations in different segments of the supply chain.